Dette and I were watching Big Bang Theory earlier tonight and the opening scene was Sheldon checking out Raj’s finances. He later on concluded that Raj cannot go to Comic-Con because he’s out of money. Prior to that episode, Raj decided that he would be a grown-up and stop asking for money from his father. So now, he is in deep debt, he’s homeless, and yeah, he can’t go to Comic-Con. Although I found the entire scene (and the episode in general) hilarious, if you think about it, Raj’s predicament really isn’t. Especially when you realise that that sort of thing actually happens to a lot of us.

So now here I am, writing another article on my blog, and wanting to talk about money.

Why talk about it?

Depending on your perspective, money could either be the most powerful tool in the world or the most evil thing invented by the human race. Or both. As a matter of fact, whether money brings people ultimate happiness or not has been a subject of debate for decades. Whatever you believe in, I think we can all agree that Money Talk is the talk that we don’t necessarily want but the one we really need.

Of course it’s safe to assume that not all of us were given the opportunity at a young age to learn about the basics of money and money management. Our parents probably didn’t want us to worry about money and our teachers in high school were more keen in teaching us what mitochondria is or what the process of turning sunlight into food is. So later on in life when we became adults and started earning money, we have no idea what to do with it.

Okay, I take that back. We have all the ideas what to do with money but most of us are clueless on how to keep it, much more make it grow.

And that is exactly why we have to talk about it.

Money doesn’t grow on trees.

Our Parents

Early experiences with money

When I finished college back in 2010, I immediately went to work. Two months after I stepped outside the gates of the University, I got a job as a programmer for a web development firm based in the US. Just to be clear though, I did not migrate to the US. Back then, the concept of “working from home” was unfamiliar to most people. So yes, I was still living in The Philippines and yet I was earning US dollars.

My life back then was a dream: I lived in our family’s home (so I did not pay any rent); I am the youngest (so I did not have any younger sibling to send to school), and; most often than not, there’s plenty of food in the pantry and the car is full of gas (so I did not have to contribute any money to the household; although thinking about it now, maybe I should have). All my salary went to my bank account.

Mine. All mine. That’s twenty thousand pesos every month. Tax free.

You would think that, with a setup like that and a very minimalist lifestyle, my savings would be ballooning and I would be traveling left and right (because, you know, travel is life) or I would be purchasing gifts for myself, my family, and our dogs here and there. Unfortunately, that wasn’t the case.

Because although I rarely bought stuff for myself and I never paid any rent nor any credit cards nor mortgages, I would still almost always run out of money days before the next salary came in. Just when I thought that I still had some money left, I don’t.

So, where does all my money go? That was the question.

Follow the money

You’ve probably heard the saying “follow the money”. If you haven’t, it’s usually said by financial investigators and/or detectives in crime and mystery movies. It means tracing the transactions and seeing where the money leads you. And wherever it does, chances are, that’s where the culprit (or the motive) is.

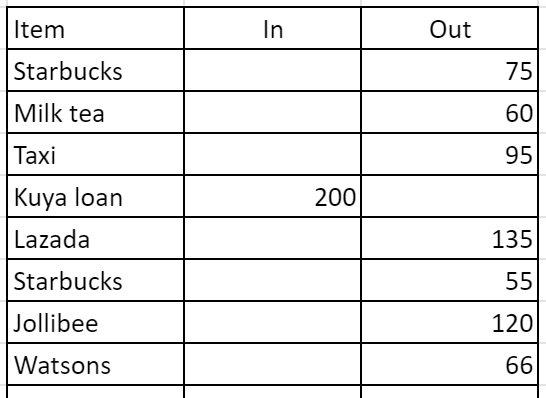

So as soon as I’m left wondering why I’m living paycheck to paycheck even with a big salary and a modest lifestyle, I knew something was wrong and something had to be done. I had to find out where my money was going. In order to do that, I went back to basic accounting: I listed all my daily expenses.

Everything. Literally.

At first, I tried doing this by mentally noting my expenses. I later on find out that this is not ideal because I have a very short-term memory and by the end of the week, my money no longer adds up. So, I got a notebook and a pen and I listed every single thing that I spent my money on. From 5-peso fares to 20-peso snacks all the way to 1000-peso Friday night outs. Everything.

If I was on the move or somewhere outside, I would list my expenses on my phone. Then I would copy them over to my notebook at the end of the day. Before the next salary, I would get the calculator and see that it all adds up.

And that is exactly the first thing that you need to do.

Write it all down

If you want to start getting a grip on your finances, the first thing you need to do is to know where your money is going. And the simplest and easiest way to do that is to list your expenses down. So go get a notebook and start writing. Get a ledger if you can.

By doing this, you achieve two things: One, you know where your money is going and that it is not magically disappearing, and; two, you can cut off spending or at least lessen your budget on unnecessary things.

And if you find writing on a notebook is too tedious, then download a money management app on your phone. You can find heaps of those online but my favourite is Expense Manager. I have been using it since forever and you can download it on Google Play. I can’t find one for iPhones but there should be something similar on the Apple App Store.

But really, it doesn’t matter what you choose to download as long as you make sure not only to use it but to use it diligently. That is, write down everything. No matter how big or how small. No excuses (yes, pati yung kwek-kwek na kinain mo kanina).

Okay, so what’s next?

Now that you’re starting to manage your expenses (money coming out) and balancing your ledger, the next thing you need to do is manage the money that is coming in. So to make sure that the money coming in is appropriated properly, you must have a budget. Ew, budget.

There are two types of budgets: fixed budget and the other one.

Fixed budgets are for things that cannot and should not be adjusted, no matter what (fixed nga eh!). Things like groceries, rent, mortgage, insurance repayments, etc. These are things that, whether you like it or not, you have to allot some amount of money to. Otherwise, you would end up like Raj: homeless, deep in debt, single, and miserable. And most often than not, these are fixed rates and paid on a regular time period.

Meanwhile, non-fixed budgets (the other one) are for things that you can go easy on. An example would be your budget for entertainment and leisure (cinema, travel, etc.), clothes, gifts, toys, etc. These are things that even if you reduce the money allotted on them, you can still survive.

You should be the one making your budget and once you have it, make sure to follow it diligently and not go over it. At the same time, review your budget every quarter to account for market fluctuation (wow, sounds so prof!).

Increasing your cash flow

If at this point you’re still running short and still (barely) living paycheck to paycheck even with a properly-crafted budget and even after reducing your expenses, then there’s one more thing you can do: multiply yourself.

No, I’m not talking about doing kage bunshin technique. What I’m saying is you should look at multiplying your sources of income (money that’s coming in). You may resort to having two jobs or taking in more shifts or renting out a bedroom in your house. But whatever it is, the goal is simple: increase your sources of income (or cash flow).

The idea of increasing your cash flow is not rocket science. I reckon a 6th grader can understand it so I don’t have to explain it to you in details.

If there’s one thing I learned about all those YouTube motivational videos I’ve watched and financial literacy podcasts I’ve listened to years ago, it’s that having one source of income isn’t enough. Sometimes you have to have two or more.

You can invest your extra dispensable money or you could learn a new skill or you could do dropshipping. I don’t know. Anything. With the advent of technology, the opportunities and the ideas are endless.

The gig economy

Back in 2019, before the whole pandemic thing, I used to drive for Uber. I would drive once a week from Friday night ’til Saturday morning or Saturday night ’til Sunday morning. Or both. The income I get out of it wasn’t luxurious but it was enough to pay my car’s weekly repayment. Plus I enjoyed driving at night in the city so that’s a bonus.

At the same time, I also have my place listed on AirBnb. I have a three-bedroom granny flat and I live by myself so it’s common sense to have my place rented out. Like Uber, the income I get from this isn’t luxurious and it’s not fixed as it’s not always booked but I earn enough that sometimes I don’t even have to spend anything on rent at all.

Other than those two, I also have my photography gig. But unlike Uber and AirBnb, this gig rarely happens. But when it does, I get to rake in big cash. Sometimes to the tune of 450$-550$ for three hours of work. Not only do I get big money, but I also get to do the thing I love most: photography. And the money I earn from this is what I save up for my photography trips/travels.

So basically, Uber is paying for my car, AirBnb is paying for my rent, and my photography is paying for my travels. My salary from my main job is then used to pay my credit card (daily expenses, bills, health plan) and the rest goes to savings. Sounds awesome, right? Yeah, and then some bloke decided to eat a bat somewhere. Now my Uber-driving, AirBnb Superhosting, and pro-photographer wannabe days are over.

Good thing I have a backup.

Your savings account is your hero

If your idea of a backup plan is your credit card, then you’re in big trouble. I think I missed to mention up there, but you should also have a fixed budget on your savings.

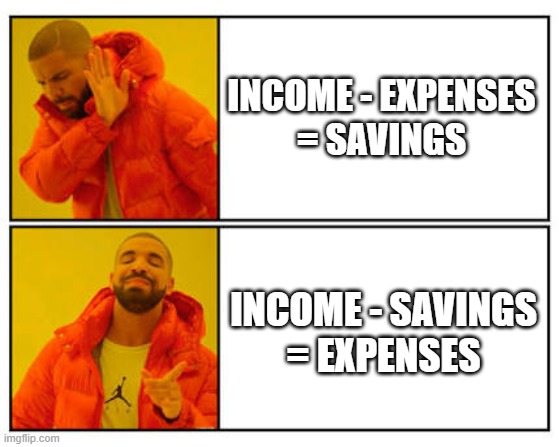

“But wait, why should I budget my savings? Shouldn’t I save what’s left after my expenses?”

No, you do not. You should instead spend what is left after saving, and not the other way around. Consider your savings as an expense to pay yourself for your services. To yourself. Yes, read that again.

This is to ensure that your savings account will always have a steady stream of money going in. And don’t fret if what you’re saving right now isn’t big yet, all that matters is that you ARE saving.

It does not matter how much you earn. What matters is how much you save.

Hernani Chua, my father

Being thrifty is not saving

Question #1: Is it saving if I’m buying discounted/cheaper/less-expensive brands?

Short answer: NO.

Long answer: NOOOOOOOOOOOOOOOOOOOOOO.

Question #2: Okay, but wait. If I’m buying this pair of shoes for 120$ instead of 250$, I’m saving 130$, right? Riiiight?

Answer: Nope. You still spent 120$.

Even if that is a much-needed pair of shoes, that could still not be counted as savings. You may have bought it for less but you still did not save anything. You were, instead, being thrifty. And being thrifty does not mean you are saving. You can only call it saving if you took out 130$ from your shoe budget and actually added it to your savings account. Still doesn’t mean you didn’t spend 120$ though.

A backup to the backup

Someone once said, “If you have accomplished all that you have planned, you have not planned enough.” I think it’s some poet or military general or something. I’m not sure. It doesn’t matter. The point is, having one backup isn’t enough. Just like your source of income, you must have two or more.

The photo above must be one of the most cliché photos on Tumblr. But just because it’s been shared gazillion times by people on social media, doesn’t mean it’s not true. So if you’re relying on your savings account alone to save you on your rainy days, you’re in trouble.

So what should be the backup to your backup then?

Life Insurance

Back in The Philippines, life insurance isn’t so popular. In fact, I know some rich families whose parents don’t even have life insurance. I’m not really sure why but maybe – just maybe – this can be attributed to the fact that there are heaps of scammers and illegal operators in The Philippines that one would really doubt about the need to have life insurance.

But, I’m telling you right now, you need one.

Why? Because life insurance is the one that’s going to save you when your savings can’t. It’s like a parachute. The first time you’re going to need it but you don’t have it, there won’t be any second time. As a matter of fact, life insurance should be the main backup and your savings the backup of the backup.

And add another backup to those two. Maybe a sugar daddy or something.

PS. your kids does not count as backups or retirement plans.

Summary

In closing, managing your finances and handling your money is actually a breeze if you know what you’re doing. It may look tedious and meticulous at first but once you get the hang of it, you’ll see that it’s a piece of cake. And with a little discipline and bit of a side hustle, you will eventually get out of the ditch you’re currently in.

So that’s it for now and I hope you picked up something valuable from this post. If you have any additions or recos for any side gigs, drop it in the comments.

Cheerio!